Key findings

Nearly 40% of investors plan to increase their private credit allocation in H1 2021, including over half (57%) of intermediaries. Private credit is also the asset class most likely to see inflows from institutional investors.

Based on surveys and interviews conducted with 65 investors in alternative assets throughout Q4 2020, Investor Intentions H1 2021 provides private credit GPs with a window into the thinking of prospective clients, and investors with critical intelligence on the plans and sentiment of peers.

Concerned by the ongoing fallout from the Covid-19 pandemic, LPs cited risk management as their number-one priority moving into 2021. Enhancing returns came next, and LPs regard private equity and private credit as the alternative asset classes most likely to deliver outperformance.

Investors were more likely to be satisfied with the performance of their private credit portfolio in 2020 than with the performance of any other alternative asset class, after the industry successfully navigated a hugely challenging market environment.

Private wealth investors gave the highest overall satisfaction rating for private credit, while asset managers and other intermediaries were most likely to be "very satisfied”.

Despite this strong demand, GPs should not become complacent. Both investors' expectations around performance and their understanding of the asset class have increased, meaning GPs' pitch to investors will also have to evolve to become more sophisticated.

Beyond superior performance, investors are also looking to private credit as a source of niche opportunities, with the asset class most likely among alternatives to be regarded as offering less commonplace opportunities to generate returns. Against a backdrop of yield compression, specialty finance vehicles pursuing strategies such as aircraft leasing are especially well placed to meet investors' needs in this regard.

As vaccination programmes gather pace throughout H1 2021, government support schemes may begin to be withdrawn. Creditors that have been sustained by such schemes could in turn experience financial distress, harming their ability to repay debts and forcing GPs to restructure deals. In this respect, ongoing transparency and communication with investors will be key to maintaining current levels of satisfaction and securing the continued growth of the industry this year and beyond.

“Both investors' expectations around performance and their understanding of the asset class have increased”

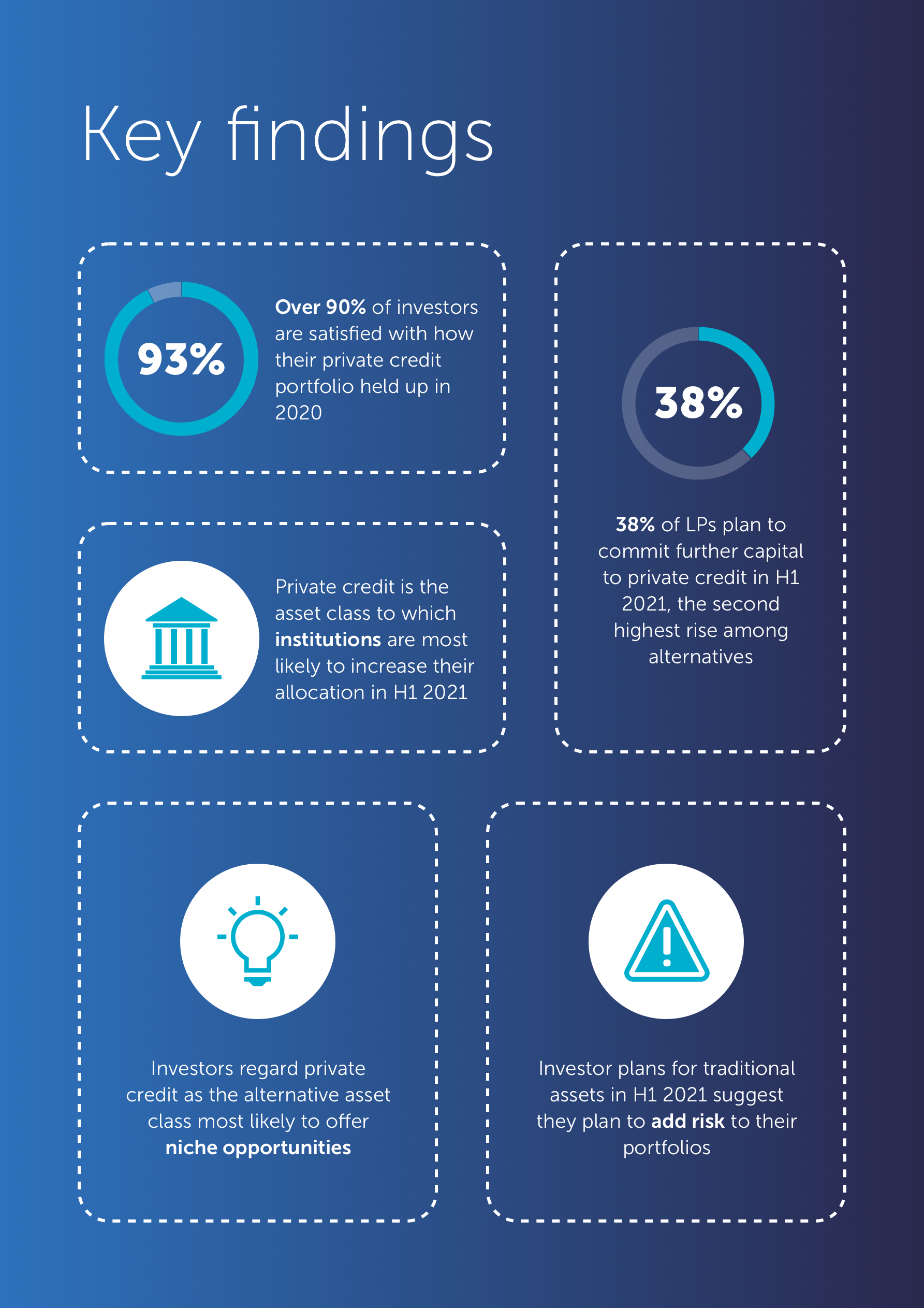

- 38% of LPs plan to commit further capital to private credit in H1 2021, the second highest rise among alternatives

- Over 90% of investors are satisfied with how their private credit portfolio held up in 2020

- Private credit is the asset class to which institutions are most likely to increase their allocation in H1 2021

- Investors regard private credit as the alternative asset class most likely to offer niche opportunities

- Investor plans for traditional assets in H1 2021 suggest they plan to add risk to their portfolios

-

Tom Kehoe

Managing Director, Global Head of Research and Communications

-

James Sivyer

Head of Investor Research, PCFI

About the research

Thanks to our participants

On behalf of PCFI and ACC, we would like to thank everyone that participated in the survey and shared their insights.

Download report

Investor Intentions H1 2021 - Private Credit Fund Intelligence is available to members and non-members of ACC. For more information about the report, please contact AIMA’s Global Head of Research and Communications, Tom Kehoe ([email protected])